I’ve seen several recent comparisons of the economies and the general quality of life on each side of the North Atlantic. Sometimes the “hook” for an article is the arrival of hundreds of thousands of Europeans in the USA for the World Cup. Other articles comment on the 10th anniversary of the Brexit vote, which could be interpreted as an attempt to shift the UK away from the EU and toward the USA.

In making these comparisons, it’s better to avoid four sources of bias:

- If you identify with the USA, the UK, or an EU country, you may be prone to defend your homeland or–if you’re like me and many Americans I know–to find reasons to criticize your own country. It’s worth trying to be relatively independent and dispassionate.

- It’s tempting to use the evidence about these countries to score points in a left-right ideological debate, assuming that the EU is left of the UK, and the USA is right of the UK. But that simplification can be misleading. The USA has a slightly higher marginal tax rate that Sweden, and about three points higher than the UK. The USA has set a lower national minimum wage than most European countries (measured by purchasing power parity), but then again, Denmark has no statutory minimum wage at all. Most European countries organize their schools using what we would call a “charter school” model, which is rare in the USA and often presented as a conservative reform here. These are examples of how policy choices vary independently of the left-right spectrum.

- We all have personal preferences for how to live. For example, I do not drive but like to live in our dense urban neighborhood, abutting restaurants and a dentist’s office. Some people prefer a lawn and a two-car garage with a basketball hoop over the door. I could try to argue for my preferences on relatively objective ethical grounds. For instance, urban living consumes less carbon. But let’s face it, my family also benefits from exclusive zoning rules. If we drop the moral comparisons and acknowledge that people value different things, then a person’s preference for life in the USA or in Europe may seem subjective.

- It’s worth separating-short term and long-term assessments. Many public goods–and ills–accumulate. For example, much of the beautiful and convenient Paris Metro system was built during the first decade of the 1900s. Its construction boosted French GDP in those years, but not now, even though Parisians still ride the Metro. In short, it is possible to live relatively well because of accumulated economic activity in the past, or to experience rapid growth now while dealing with deficits and liabilities.

I suppose my bottom line would be that some aspects of human development are better in the EU than in the UK, and in the UK compared to the USA, but a surprising number of such comparisons are quite close. At the same time, the USA has seen substantially stronger annual economic growth during the 21st century. One can argue for a steady-state economy (or at least criticize GDP growth as a measure of success), but the actual political and economic systems–on both sides of the Atlantic–currently depend on annual growth. Thus the EU faces a current challenge that is mitigated by its accumulated investments.

To elaborate:

Life expectancy in the US is about two years lower than that in the UK and the EU.

The intentional homicide rate in the US is five times higher than that in the UK and 5.7 times that in the EU.

Educational attainment/investment varies widely within the EU. The average number of years of formal education in both the USA and Germany is 13.8; in the UK, 13.2; and in Italy, 10.

On the most popular measure of income inequality (GINI), the USA ranks worse than the UK, which ranks worse than the EU. (The respective scores are 39.6 for the USA, 34.2 for the UK, and 29.4 for the EU.) There is wide variation within the EU zone, but the least equal European countries–Portugal, Spain, and Italy–are more equal than the UK.

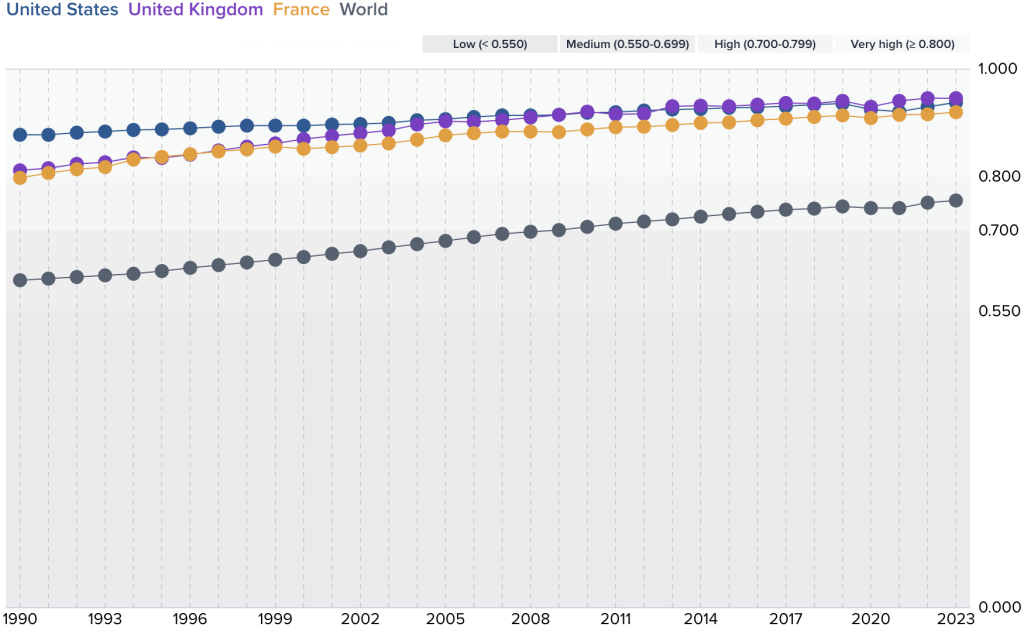

By the overall measure of the Human Development Index, the USA comes in just ahead of Britain, which is just ahead of the EU. (I show France below because the HDI website won’t generate a line for the EU, and France is at the EU mean right now.) However, HDI includes per capita income, which is much higher in the USA. Europe’s HDI is pushed higher by life expectancy and education. To put it another way, EU countries achieve similar health and educational outcomes as the USA with much less wealth.

Meanwhile, here is a comparison of economic growth (change in real gross GDP) for the USA, the United Kingdom, and the EU. I’ve set each trend-line at 100 on the Millennium, so that you can compare relative change since then in each of these markets.

(On a per capita basis, GDP has been quite different all along, reaching about $94k in the United States, $61k in the United Kingdom, and $51k the EU in 2026.)

Although I remain convinced that Brexit was disastrous for the UK, it is interesting that the UK economy has grown more than the EU has since 2020.

The sharp contraction caused by COVID was worst in the UK, although their recovery was larger than the EU’s. The COVID contraction was distinctly smaller in the USA. We lost four years of GDP in 2020, whereas the UK temporary lost 15 years of growth at the nadir of the pandemic.

Since 2020, the US has seen substantial growth: steady increases except for one quarter in early 2021. The line is basically straight through Biden and Trump II. Both the UK and EU pulled out of COVID and then experienced basically a plateau.

This doesn’t mean that life is worse in the EU. Europe is much less violent, and the amenities and public goods that I value are more plentiful there. But the lack of growth poses a challenge, given the logics of the EU’s political and economic systems.

See also: Brexit: a personal reflection (2019); the UK in a polycentric Europe; reflections on modern Granada (Spain); the international variation in COVID-19 mortality etc.